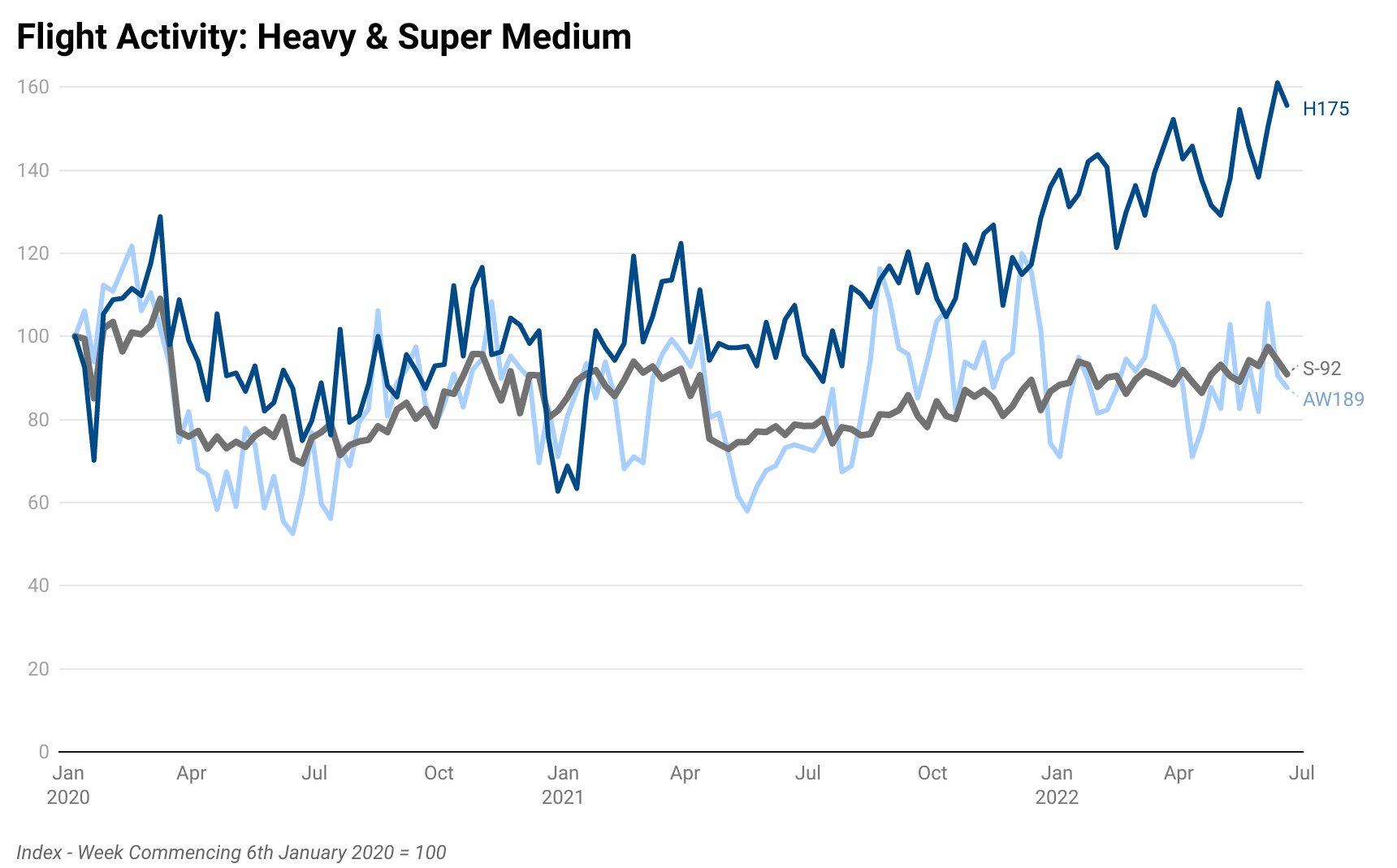

The latest census of active offshore crew transfer helicopters in the heavy & super-medium segment shows a substantial recovery in active aircraft and number of flights flown. Analysis of activity for each helicopter operating in the offshore crew transfer fleet shows a net year-on-year improvement of 5% in the active fleet of aircraft. OMNI and PHI have seen the most growth in active heavy & super-medium offshore rotorcraft, with a net increase in active aircraft in this weight category of six each. Bristow, in contrast, has seen its active heavy & super-medium fleet reduce by 7 units (all S-92s.) Analysis of flight activity as of June 2022 shows that the overall weekly number of heavy & super-medium flights has recovered to in excess of pre-Covid (January 2020) levels with the H175 fleet seeing flight activity up over 50%. These are amongst the headline findings of the latest “S-92 Fleet Census” released today by research firm Air & Sea Analytics.

Director Steve Robertson remarked “The uplift in active aircraft is not surprising given high oil prices and double-digit growth in upstream expenditure. Of particular interest is the underlying intensity of activity in returning aircraft to service (RTS). Aircraft that a year ago no-one would have expected to return to the active fleet are now flying again.

“It’s only a matter of time before scarcity of available aircraft and parts drives up pricing significantly”

Whilst there were still 41 inactive S-92s in Q1 2022, the reality for anyone trying to source an aircraft just now is that AW189s and H175s are at or near full effective utilisation and the pool of available S-92s is less than two dozen when you account for RTS activity, secondary market activity and retirements already underway. Interviews conducted during the preparation of the report highlighted supply chain bottlenecks in the provision of aircraft parts and workshop capacity for return-to-service programs.”

We review the fleet unit by unit and share and sense check our outputs on the same basis with the OEMs, Lessors and others. The S-92 market has been subject to arbitrary speculation for years. The purpose of this analysis is to provide an objective, data-driven, independent view and to evaluate the demand-side (i.e. the number of units flying) rather than cover the supply side (fleet).”

The legacy of the 2016 and 2019 bankruptcies in this market is starting to fade: we no longer have a large number of inactive assets owned by banks, these have been moved on into the hands of operators and lessors that can put them to work. Recent acquisitions in the last year include three S-92s acquired by Milestone from Capital One and two units acquired by CHC from PNC. That said, the financial health of the offshore helicopter operators is a mixed picture, whilst PHI have reported excellent results for 2021 and a strong Q1, we note others such as Caverton have reported the opposite.”

The ‘Heavy & Super-Medium Fleet Census’ report, available now via Air & Sea Analytics, evaluates rotorcraft usage by country and operator, showing the current position vs previous census a year prior. A unit-by-unit breakdown is provided by serial number showing location and status.

The consequence of eight years of low oil prices and oil company capital discipline is underinvestment in oil production capacity. Oil prices have subsequently recovered as spare production capacity is eroded. A new oil cycle is underway as the market seeks to bring new capacity to market. Upstream expenditure is expected to increase nearly 20% in 2022 to reach $420bn. This is driving increased field exploration and development activity which requires aircraft for offshore personnel transfer.

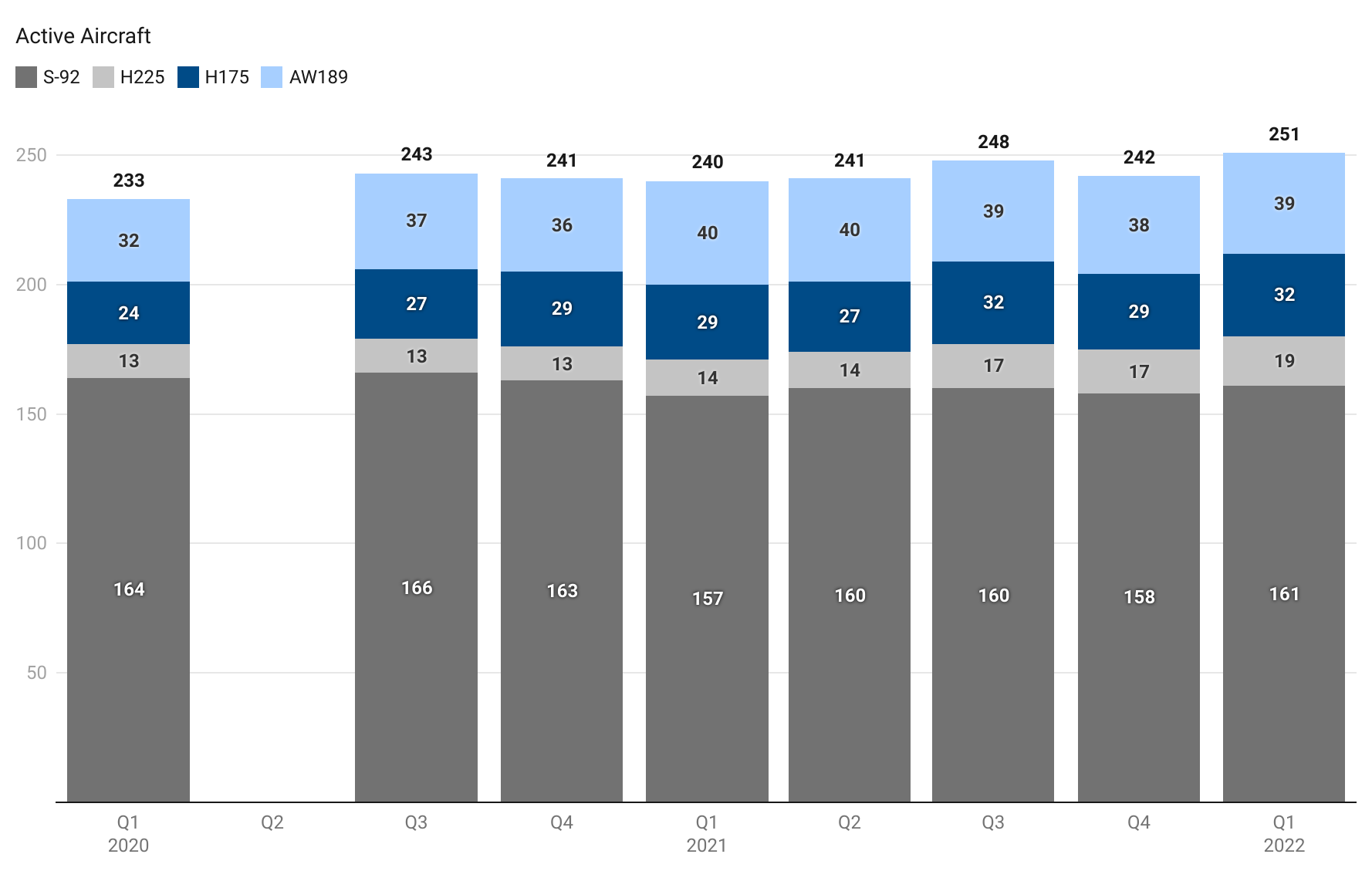

The last published census of S-92 units showed 157 working in March 2021 and since then we have seen recovery in the market with 161 now active as of March 2022. In other heavy and super-medium types we note 19 active offshore H225s, 32 H175s and 39 AW189s. (We expect sanctions imposed on Russia recently to ultimately impact AW189 utilisation as a third of the active units are located in Russia and will be unable to source spare parts from Italy)

For more information please contact us or click on the report cover to the right.