VAI 2026

Atlanta hosted the rotorcraft industry's annual gathering last week, and as the dust settles on three days of announcements, three themes stand out — not just as show news, but as signals about where this industry is heading.

1. Autonomy Is No Longer a Concept — It's a Product

Verticon 2026 will be remembered as the show where rotorcraft autonomy moved from the future pavilion to the main floor.

The most striking debut was Robinson's R66 "TurbineTruck" — an unmanned cargo variant of the world's most popular turbine helicopter, built around Sikorsky's MATRIX autonomy system. This is no skunkworks experiment. Robinson has formally launched a dedicated unmanned subsidiary, Robinson Unmanned, incorporating Ascent AeroSystems (acquired in 2024) alongside unmanned derivatives of both the R44 and R66. The TurbineTruck carries a 1,500 lb (680 kg) useful load — split between fuel and cargo — and is capable of both remote piloting and full autonomous flight. The platform targets military logistics, disaster relief, and civil utility work. MATRIX, previously demonstrated on the S-76 and UH-60 Black Hawk, has now been scaled down to a commercially accessible, high-volume airframe. That matters enormously. If MATRIX on a Black Hawk was a proof of concept, MATRIX on an R66 is a market entry.

On the fixed-wing VTOL side, Airbus used Verticon to announce that Garuda Technologies — an Indian-American UAS company with over 5,000 drones deployed and 30% dominance in India's agricultural drone market — has selected the Flexrotor for up to 18 aircraft. Airbus acquired the Flexrotor (originally developed by Aerovel) in 2024. The system is a tilt-rotor UAS: it takes off vertically from a 3.7 x 3.7 m footprint, transitions to fixed-wing cruise, and can carry an 8 kg payload for 14 to 30 hours. Garuda will offer it on both dry and wet lease terms across infrastructure inspection, law enforcement, wildfire monitoring and disaster relief.

Two different philosophies — one large and autonomous, one small and persistent — but the same direction of travel. The lines between helicopter OEMs and UAS companies are dissolving.

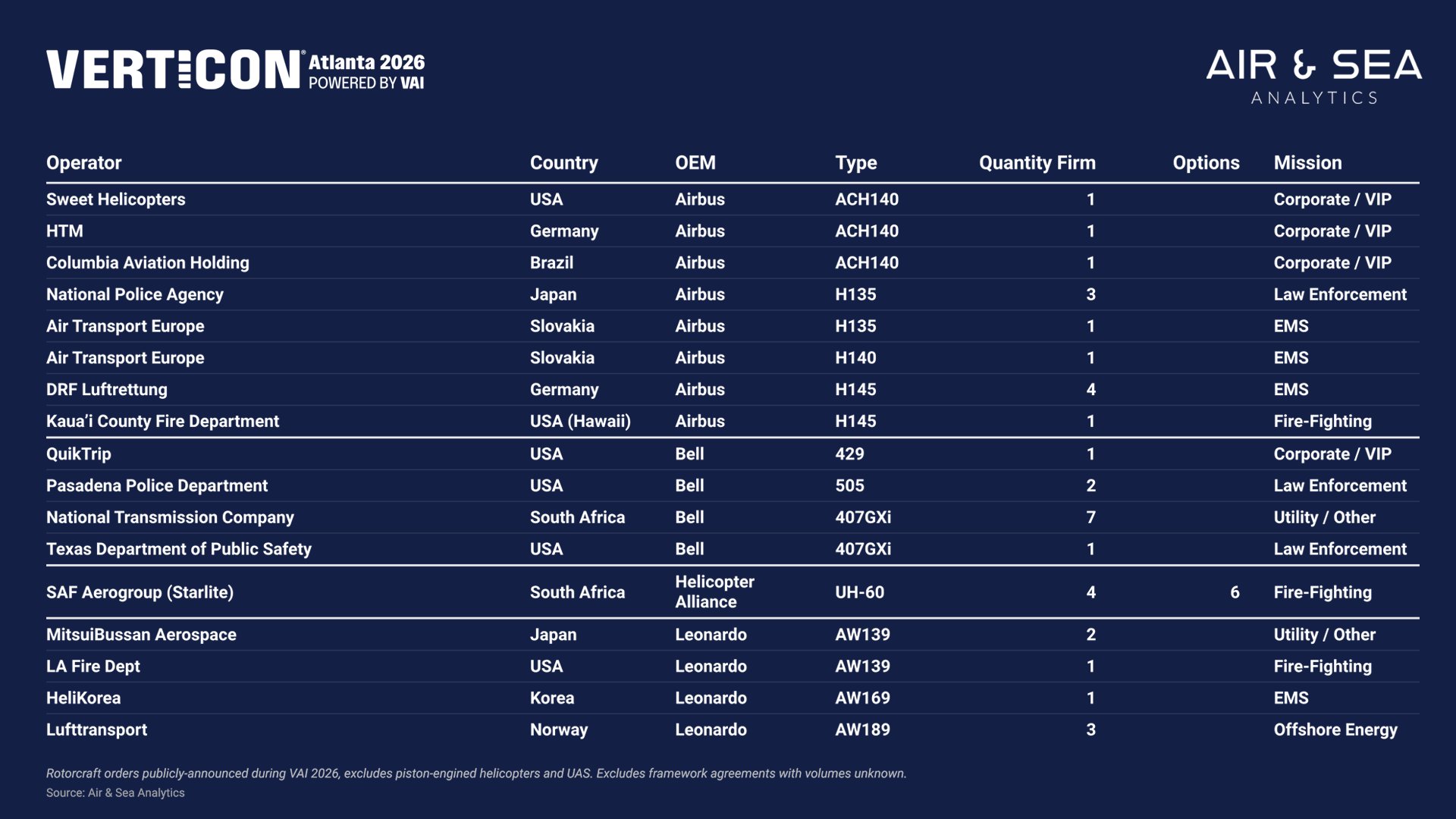

2. HEMS Is Now Driving the Orderbook

Cast an eye across the publicly announced orders at Verticon 2026 — 35 firm commitments and one mission type (other than the broad utility segment) dominates: Emergency Medical Services.

ADAC Luftrettung, Europe's largest HEMS operator with 37 bases and approximately 50,000 annual missions, signed a long-term framework contract for H135, H140 and H145 aircraft, cementing its role as both a launch customer and development partner for the new H140. Air Transport Europe of Slovakia added one H135 and one H140 for operations across challenging mountainous terrain in Central Europe. HeliKorea — the leading private helicopter operator in South Korea — ordered a further AW169 to expand its EMS fleet, following three units placed in 2025.

It is also worth noting that DRF Luftrettung, the German air rescue organisation, placed an order for four H145s — the latest in a long succession of buys that have made the H145 the default EMS platform across Germany.

The HEMS demand signal is not new, but its weight in the Verticon orderbook is striking. In a show that produced 35 firm orders, EMS-related commitments accounted for a significant proportion — and they spanned two OEMs and four operators across five countries. The driver is well understood: an ageing European population, expanded national air ambulance coverage, and the helicopter's irreplaceable role in time-critical trauma response.

3. The S-92 Is Back! But not as you know it…

The S-92 is known as the workhorse of the offshore industry but deliveries tailed off in the oil industry downturn post 2015 and the last MSN delivered to the energy industry was 920310 in 2020 to Chevron. There has been an expectation that the S-92 would exit the offshore market fairly quickly over the next two decades but thus far the S-92 has been enjoying good availability and even the aircraft displaced by super-mediums have found work elsewhere.

A week before the show, Sikorsky announced it is ramping up production of the upgraded S-92A+ — and the headline customer is not an offshore operator, but a Head of State transport user. A 14th country has ordered two S-92A+ aircraft for government transport, following deliveries to two Head of State customers in Asia and the Middle East in 2025. Sikorsky is standardising all new production around the A+ model, which features a Phase IV main gearbox — the most technologically advanced commercial helicopter gearbox currently in production — along with upgraded engines. Production capacity stands at up to 12 aircraft annually.

This is a meaningful pivot. Head of State and VVIP operators choose the S-92 for reasons that are distinct from the offshore calculation: range, cabin volume, reliability (it holds the highest heavy commercial helicopter flight hours record), and — crucially — the prestige of the presidential pedigree, having underpinned 23 VH-92A aircraft for US presidential transport. The platform's military credibility translates directly into diplomatic procurement.

The noteworthy signal here is what is not happening: the S-92 is not winning new offshore energy contracts at scale. Lufttransport's order for three AW189s at Verticon — the only offshore energy order of the show — is a reminder of where the super-medium market's centre of gravity sits. But Sikorsky appears to have found a sustainable niche in the heavy segment that does not require competing with the AW189 on the Norwegian Continental Shelf. Government transport is a smaller market, but it is consistent, high-value, and largely insulated from the oil price cycle.

The S-92 is not staging a comeback. It is finding a new identity.

Steve Robertson

Air & Sea Analytics