The 2026 Iran War: A Systemic Shock to the Global Energy Complex and Its Cascading Economic Consequences

Summary

The US-Israeli military operation against Iran, launched on 28 February 2026, has triggered what the International Energy Agency has described as "the largest supply disruption in the history of the global oil market." Iran's retaliatory closure of the Strait of Hormuz — through which approximately 20% of global oil and one-fifth of the world's LNG transits daily — has produced a supply shock of a magnitude not seen since the 1973 Arab oil embargo, with effects that are arguably more severe given the interconnectedness of the modern global economy.

One month in, the consequences are no longer theoretical. Brent crude has surged above $100/bbl from a pre-war ~$67, global oil supply has been reduced by an estimated 11 million barrels per day net of mitigation measures, sovereign governments are implementing wartime-style fuel rationing, and critical downstream industries — from fertilisers to petrochemicals to aviation — face supply chain fractures that will take years to fully repair.

This article examines the economic architecture of the disruption across four dimensions: the macro oil and gas supply shock; the cascading impact on adjacent industries including petrochemicals, fertilisers, and food security; demand-side measures being deployed by governments worldwide; and the impact on upstream oil and gas operations and the offshore helicopter industry in the GCC states.

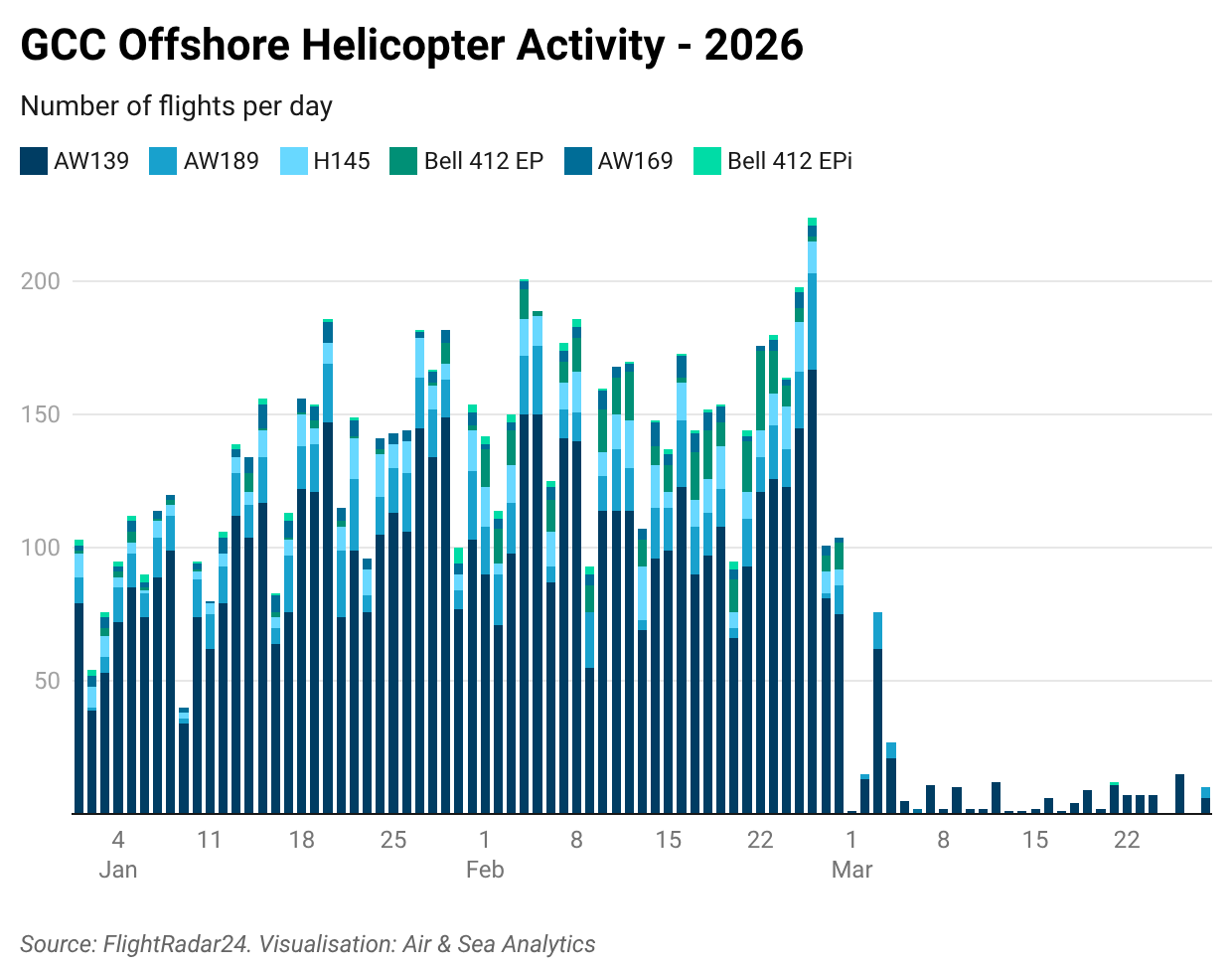

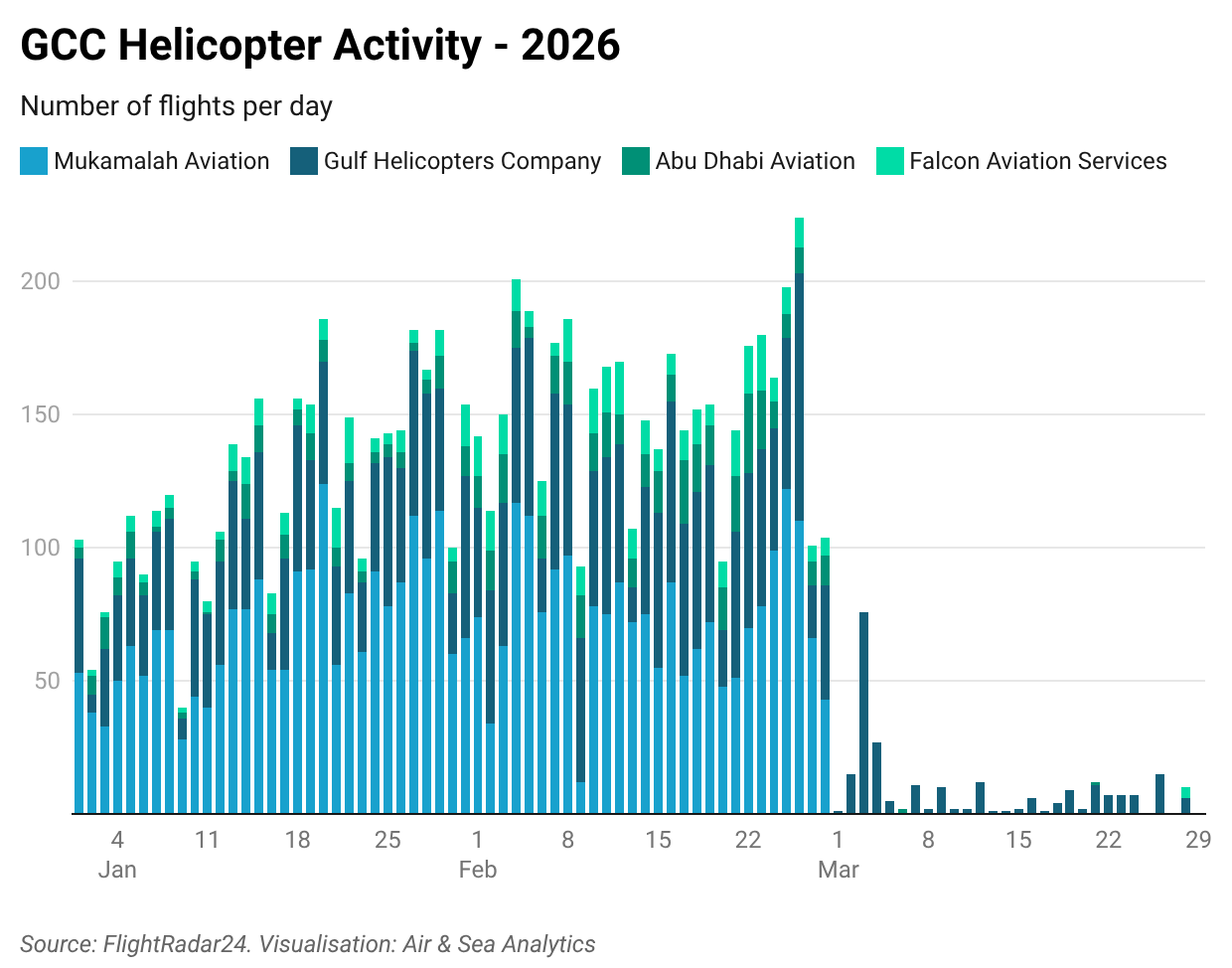

Middle East Helicopter Flight Activity per day by Helicopter Type, January - March 2026

I. The Oil and Gas Supply Shock

The Strait of Hormuz: A Chokepoint Without Substitute

In 2025, approximately 20 million barrels per day of crude oil and refined products transited the Strait, alongside significant LNG volumes — primarily from Qatar. Iran's effective closure to Western-aligned shipping has removed the equivalent of roughly one-fifth of global oil consumption from trade flows.

Pre-war daily exports through Hormuz (IEA, 2026):

• Saudi Arabia: 6.23 mb/d

• Iraq: 3.63 mb/d

• UAE: 3.24 mb/d

• Kuwait: 2.37 mb/d

• Iran: 2.41 mb/d

• Qatar: 1.43 mb/d

• Bahrain: 0.21 mb/d

• Total: ~20.0 mb/d

Saudi Arabia's East-West pipeline to Yanbu and the Abu Dhabi Crude Oil Pipeline to Fujairah provide a combined bypass capacity of ~6.5 mb/d — barely one-third of normal Hormuz throughput.

Price Impact

Brent surged to $126/bbl within the first ten days, has traded above $100 since mid-March, and some analysts are modelling $200/bbl scenarios if closure extends 3–4 months. Bloomberg estimates a net daily supply shortfall of ~9 million barrels after accounting for SPR releases and bypass flows — a gap exceeding the combined daily consumption of the UK, France, Germany, Spain, and Italy.

More than 30 countries agreed on 12 March to release a record 400 million barrels of strategic reserves. At current drawdown rates, this provides weeks of buffer, not months. Europe faces diesel shortages within weeks if the Strait remains closed.

Natural Gas

Qatar declared force majeure on all LNG shipments on 4 March after Iranian strikes on Ras Laffan. LNG exports from Ras Laffan account for 20% of global LNG trade. Asian LNG spot prices have surged 60%. Iran's South Pars field has also been struck by Israeli attacks (South Pars and Qatar’s ‘North Dome’ are a single giant hydrocarbon structure than spans the border - the largest gas field in the world.)

II. Cascading Impact on Adjacent Industries

Petrochemicals

The Middle East is the world's lowest-cost petrochemical production hub. SABIC has curtailed output at several Saudi facilities. Abu Dhabi's Borouge has reduced production. Iran's petrochemical sector — $14bn in export revenues in 2025 — has been devastated by strikes on Kermanshah, Shiraz, and the Mahshahr Industrial Complex. Downstream effects span plastics, synthetic fibres, rubber, solvents, adhesives, and pharmaceuticals globally.

Fertilisers: A Food Security Crisis in Formation

This is perhaps the most consequential — and least reported — aspect of the disruption. The Middle East accounts for ~35% of global seaborne urea exports and ~45% of global sulphur exports.

Key price movements (S&P Platts):

• Middle East granular urea: $435–490/t pre-war → $604–710/t by 19 March

• Futures (next-month delivery): $475 on 27 Feb → $745/t

• NOLA urea barges: up $60–80/t in the first two weeks of March alone

QatarEnergy's force majeure has halted QAFCO — the world's largest single urea production complex. Three Indian urea plants have curtailed output due to LNG supply constraints. Natural gas comprises 60–80% of ammonia production costs, making fertiliser prices acutely sensitive to this shock.

Timing is catastrophic — the Northern Hemisphere spring planting window is open now. Yara CEO Svein Tore Holsether: "If you're not getting fertiliser into the field of the farmers, yields could go down by up to 50% in the first harvest." Russia stands to benefit materially as an alternative supplier — Baltic FOB urea has climbed from ~$375/t in 2025 to $563–586/t.

Shipping and Insurance

War-risk insurance premiums for vessels in the Persian Gulf have surged to prohibitive levels. At least 27 commercial vessel attacks have occurred since 28 February. Over 150 tankers are anchored outside the Gulf unable to secure insurance coverage.

III. Demand-Side Measures: The Return of Wartime Economics

The supply shock has forced governments worldwide into emergency demand management not seen at this scale since the 1970s. Asia is the frontline — Japan and South Korea source 90% and 70% of their crude from the Middle East respectively.

Philippines: Four-day work week for civil servants mandated; private sector encouraged to follow. AC capped at 24°C; state of national emergency declared.

Sri Lanka: Every Wednesday declared a public holiday for government workers. Nationwide fuel rationing — motorists limited to 15 litres/week, motorcyclists to 5 litres. Universities moved online.

Pakistan: Schools closed two weeks from 16 March. Government workers on four-day week. 50% of staff working from home. Government spending cut 20%; 60% of official vehicles taken off the road.

Bangladesh: Fuel rationing from 8 March. Universities closed. ~95% energy import dependent — facing rolling power cuts.

Thailand / Vietnam: Government WFH mandates; Thailand's PM asked officials to use stairs not lifts. Fuel price caps in both countries.

India: Essential Commodities Act invoked to prioritise household LPG over commercial users. Minimum 25-day gap between cylinder bookings imposed.

China: Ban on refined fuel exports to prevent domestic shortages.

Slovenia: First EU member state to introduce fuel rationing — motorists capped at 50 litres/day; businesses at 200 litres.

Ireland: €235m package — excise cuts of 15c/litre petrol, 20c/litre diesel; NORA levy suspended; welfare heating payments extended.

UK: Petrol at 18-month highs. Government monitoring for profiteering; £53m package for low-income heating oil users. A second COBRA meeting convened 30 March.

Australia: Free public transport in Victoria and Tasmania to reduce driving demand.

Egypt: Mandatory closure of shops, restaurants, and shopping centres from 9pm nightly.

IV. Upstream Oil and Gas: Shutdowns, De-Manning, and Infrastructure Damage

Saudi Arabia

Aramco has cut production by 2 million bpd to ~8 million bpd after shutting the supergiant Safaniya and Zuluf offshore fields. The 550,000 b/d Ras Tanura refinery has been suspended. Onshore tank farms at Ras Tanura, Ju'aymah, and Dhahran reached ~85% capacity within ten days of the conflict, forcing proactive output cuts simply to avoid physical overflow.

UAE

ADNOC has shut the 922,000 b/d Ruwais refinery. The Fujairah export terminal has come under repeated attack. UAE daily oil output has more than halved. TotalEnergies reported 15% loss of its Middle East upstream output by 12 March.

Iraq

Southern field output cut 70% — from 4.3 mb/d to 1.3 mb/d. Northern Kirkuk-Ceyhan pipeline to Turkey being used for partial rerouting but capacity is limited.

Kuwait / Qatar / Bahrain

Kuwait Petroleum Corporation declared force majeure 7 March. Qatar halted all LNG operations and declared force majeure 4 March. Bapco Energies (Bahrain) declared force majeure 9 March after the Sitra refinery was struck.

Platform De-Manning

Non-essential personnel have been evacuated from offshore installations across Saudi Arabia, the UAE, and Kuwait. Drilling programmes have been suspended or scaled back to skeleton crews. Arabian Drilling, ADES Holding, and Borr Drilling have all formally announced temporary suspensions of offshore rig operations — the latter down-manned three jack-up rigs in Qatar and the UAE at customer request.

The medium-term damage extends beyond immediate production losses. Deferred maintenance on ageing offshore infrastructure risks accelerating decline rates. Bloomberg and Chatham House both conclude that full recovery of Gulf energy production capacity will take years, not months, even after hostilities end.

V. Impact on the GCC Helicopter Industry

The GCC civil helicopter market is one of the world's most concentrated offshore aviation markets. Primary demand drivers are offshore oil and gas crew transfer operations and mega-project logistics under Vision 2030 and equivalent UAE programmes. Key operators include Abu Dhabi Aviation, Gulf Helicopters (Qatar), and Saudi-based Mukamalah.

The Impact of the Conflict

The conflict has effectively shut down routine offshore helicopter operations across much of the GCC:

Demand collapse: With platforms de-manned and production suspended across Saudi Arabia, UAE, Kuwait, and Qatar, crew transfer flying — the core revenue base for Gulf helicopter operators — has ceased or been sharply reduced to emergency-only operations.

Middle East Helicopter Flight Activity per day by Operator, January - March 2026

Airspace restrictions: Iranian missile and drone strikes on all six GCC member states triggered airspace closures and severely constrained available corridors. Seven Gulf nations restricted airspace in the first week of the conflict.

Military requisition: UAE Apache squadrons have been redeployed to air defence duties, successfully intercepting Iranian Shahed-136 kamikaze drones with 30mm cannon and APKWS rockets. The UK is deploying Wildcat and Merlin helicopters for anti-drone roles. Military rotary-wing demand has surged as civilian demand has collapsed.

Insurance repricing: War-risk aviation premiums have escalated sharply, making non-essential operations prohibitively expensive even where airspace permits.

Supply chain disruption: Components, MRO resources, and spare parts supply chains face delays and cost escalation.

Market Outlook

Even in an optimistic ceasefire scenario, the helicopter market faces a protracted recovery:

• Production restart timelines for offshore fields are measured in months — crew transfer demand will not snap back

• Insurance markets will carry elevated Gulf aviation risk pricing for years

• IOC and NOC capex deferrals on Gulf upstream projects will suppress medium-term demand

• Vision 2030 and UAE development programmes may face funding constraints as sovereign wealth funds redirect capital to reconstruction

The conflict may also accelerate the transition to unmanned systems — evidenced by the UAE's January 2026 order for 168 ANAVIA unmanned helicopters for military logistics and ISR, signalling where capital is now being directed.

VI. Conclusion: A Structural Repricing of Risk

The 2026 Iran war has shattered the foundational assumption of modern energy markets — that the Strait of Hormuz, however threatened, would never actually close. It has. The economic consequences span crude oil, LNG, petrochemicals, fertilisers, food security, shipping, and aviation.

For the energy industry specifically:

• Diversification away from Gulf dependency will accelerate, benefiting US shale, Guyana, Brazil, and West Africa, and fast-tracking investment in renewables and nuclear.

• Strategic reserve policy will be comprehensively reviewed — the current system has bought time but exposed fundamental inadequacy for a disruption of this scale.

• The energy security premium will be structurally repriced into sovereign planning and corporate strategy for a generation.

• The GCC's diversification imperative — already urgent — becomes existential.

As Bloomberg concluded on 29 March: if the Strait remains closed, the world must "significantly reduce its oil and gas consumption — but not before prices spike to a level that forces consumers and businesses to fly, drive and spend much less."

The question is no longer whether this conflict reshapes the global energy order. It is how profoundly, and for how long.